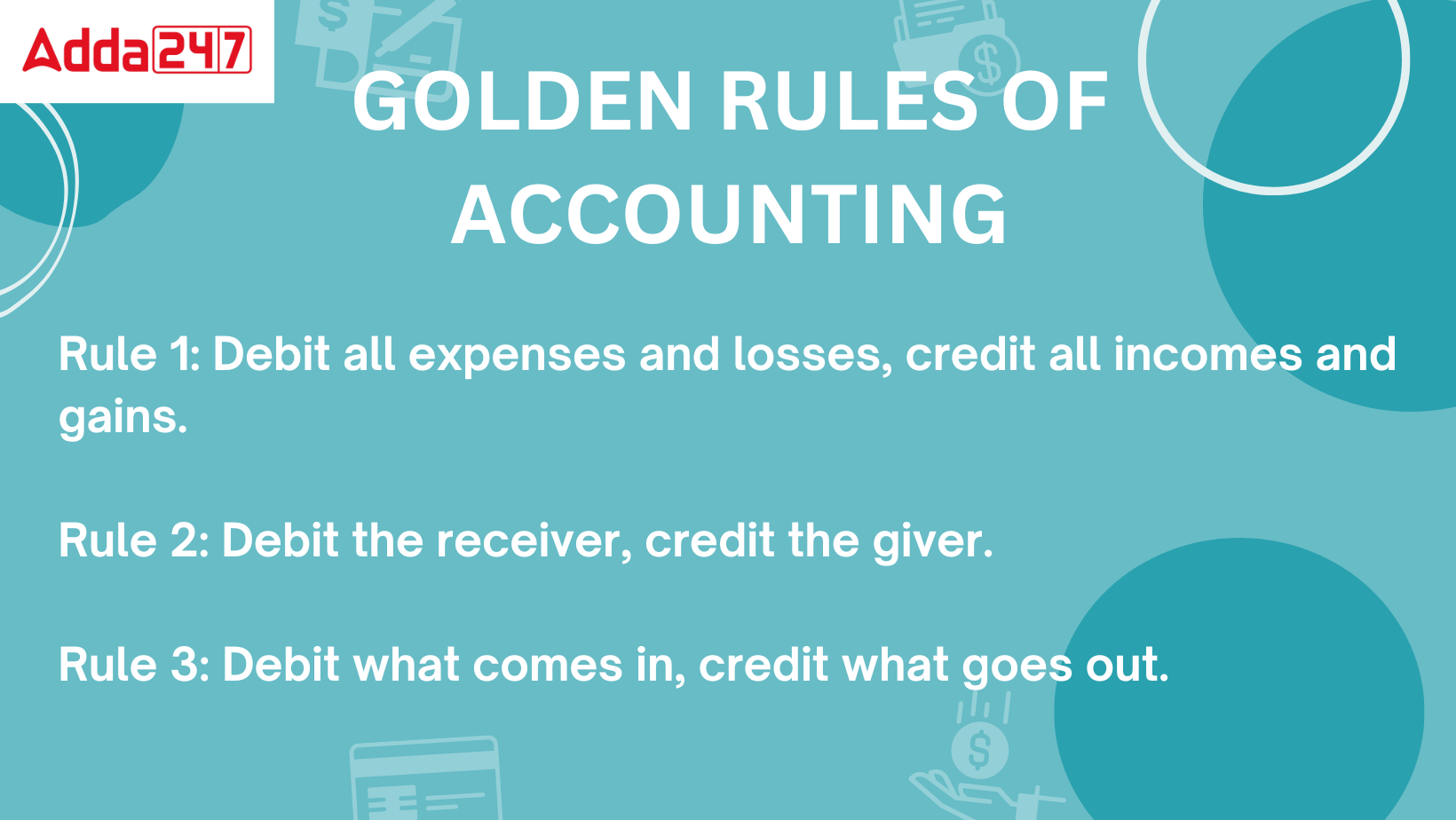

Golden Rule of Accounting

Bookkeeping is only one aspect of financial accounting. Every transaction in accounting has a debit and a credit entry. Knowing which account needs to be credited and which one needs to be debited is important. This is the dual-entry accounting method. The three principles that make up the “golden rules of accounting” govern financial accounting. The methodical recording of financial transactions is ensured by these golden principles. The golden rules reduce the intricate bookkeeping regulations to a collection of straightforward concepts that may be learned and used.

3 Golden Rules of Accounting

The Golden Rules of Accounting, also known as the Three Golden Rules, are fundamental principles that form the basis of the double-entry bookkeeping system. They help maintain the integrity and accuracy of financial transactions recorded in the accounting books. The three Golden Rules are as follows:

- Debit what comes in, Credit what goes out: This rule applies to transactions involving real accounts, such as assets and liabilities. When an asset (something of value owned by the business) increases, it is debited. On the other hand, when a liability (something the business owes) increases, it is credited.

- Debit the receiver, Credit the giver: This rule applies to transactions involving personal accounts, such as individuals or entities with whom the business has financial dealings. When a business receives money or benefits from a person or entity, that person’s account is debited. Conversely, when a business gives money or benefits to a person or entity, that person’s account is credited.

- Debit all expenses and losses, Credit all incomes and gains: This rule applies to transactions involving nominal accounts, which include revenues, expenses, gains, and losses. When the business incurs expenses or experiences losses, those accounts are debited. On the other hand, when the business earns income or gains, those accounts are credited.

It is important to note that these rules are based on the double-entry bookkeeping system, where every transaction is recorded in at least two accounts with equal debits and credits. This ensures that the accounting equation (Assets = Liabilities + Equity) remains in balance and helps prevent errors and fraud in financial records. The Golden Rules are universally followed in accounting practices to maintain consistency and accuracy in financial reporting.

Golden Rules of Accounts Types

Ledgers are used to record financial transactions in accordance with the accounting profession’s golden principles. These guiding principles depend on the kind of account. Each transaction will have a debit and credit entry and be associated with one of the accounts listed below. There are three types of accounts:

- Real Account

- Personal Account

- Nominal Account

Real Account

A real account is a general ledger account that records all asset and liability-related transactions. Both actual and intangible assets are included. tangible goods like furniture, real estate, a building, equipment, etc. In contrast, intangible assets like goodwill, copyright, patents, and so forth

Real accounts are not closed at the conclusion of the fiscal year since they are carried over to the next one. The balance sheet also includes an actual account. Real accounts include furniture accounts.

Personal Account

A general ledger account pertaining to people is a personal account. It may be artificial or genuine persons, such as companies, firms, associations, etc. Company A becomes the receiver when it is given money or credit by another company or person. In the event of a personal account, the other company or person who donates it also assumes the role of the donor. One kind of personal account is a creditor account.

Nominal Account

A nominal account is a general ledger account that records all revenue, costs, profits, and losses for a company. It records every transaction relating to a single fiscal year. The balances are therefore reset to zero and may now begin again. One kind of nominal account is an interest account.

Golden Rules of Accounting with Examples

The foundation of bookkeeping are the golden rules of account. You must identify the type of account for each transaction in accordance with the golden standards of accounting. There are specific guidelines for each type of account that must be followed for every transaction. The three guiding principles of accounting are as follows:

Golden Rule of Accounting Rule 1: Debit What Comes In, Credit What Goes Out

This regulation is applied to real accounts that include tangible assets such as equipment, buildings, land, furniture, etc. By default, they have a debiting balance, which debits all incoming funds and adds them to the account balance.

Similar to this, when a physical asset departs the business, the account balance needs to be credited.

Example:

You purchased furniture for Rs. 2,5000 in cash. Debit your Furniture Account (what comes in) and credit your Cash Account (what goes out).

| Date | Account | Debit | Credit |

|---|---|---|---|

| XX/XX/XXXX | Furniture Account | 25000 | |

| Cash Account | 25000 |

Golden Rule of Accounting Rule 2: Debit the Receiver, Credit the Giver

For personal accounts, the “Debit the receiver, Credit the giver” rule is in effect. Donations to a business, whether made by a natural or artificial entity, are referred to as inflows. As a result, the company receiving the donation must be credited in the books and the receiver must be debited.

You purchase 5000 worth of goods from Company XYZ. In your books, you need to debit your Purchase Account and credit Company XYZ. Because the giver, Company XYZ, is providing goods, you need to credit Company XYZ. Then, you need to debit the receiver, your Purchase Account.

| Date | Account | Debit | Credit |

|---|---|---|---|

| XX/XX/XXXX | Purchase Account | 5000 | |

| Account Payable | 5000 |

Golden Rule of Accounting Rule 3: Debit All expenses and Losses, Credit all Incomes and Gains

Nominal accounts are covered under this golden accounting rule. It has a credit balance because it views the capital of a corporation as a liability. As a result, when gains and income are credited, the capital will rise. Conversely, when losses and expenses are deducted from it, this capital is decreased.

Example:

You purchase 6,000 of goods from Company. To record the transaction, you must debit the expense (6,000 purchase) and credit the income.

| Date | Account | Debit | Credit |

|---|---|---|---|

| XX/XX/XXXX | Purchase Account | 6000 | |

| Cash Account | 5000 |

Golden Rules of Accounting PDF

Golden Rules of Accounting PDF To download this PDF of 3 golden rules of Accounting Click on the Link.

CLAT 2027 Preparation: Complete Study Pl...

CLAT 2027 Preparation: Complete Study Pl...

Best CLAT Online Course 2027: Why Adda24...

Best CLAT Online Course 2027: Why Adda24...

Best Strategy to Attempt the CUET Exam f...

Best Strategy to Attempt the CUET Exam f...