Correct option is A

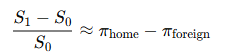

Relative PPP focuses on changes in exchange rates over time and how they are driven by inflation differentials between two countries. According to this theory, if one country experiences a higher rate of inflation than another, its currency should depreciate relative to the other to maintain parity in the purchasing power.

Mathematically, the percentage change in the exchange rate between two currencies over time is approximately equal to the difference in the inflation rates of the two countries:

Where:

S0 is the initial spot rate

S1 is the future spot rate

πhome and πforeign are inflation rates in the home and foreign countries respectively

Thus, Relative PPP captures the dynamic relationship between inflation and currency depreciation over time, unlike Absolute PPP which is static and theoretical in nature.

Information Booster:

Relative PPP explains the movement of exchange rates in response to inflation rate differentials.

It helps in forecasting future exchange rates using inflation projections.

This theory is widely used in long-term exchange rate modeling.

It assumes freely floating exchange rates and absence of government intervention.

Relative PPP is more realistic than Absolute PPP as it accounts for real-world inflation effects.

It supports the International Fisher Effect, which links interest rates and exchange rates.

Useful for MNCs and investors to hedge exchange rate risk in long-term contracts.

Additional Knowledge:

(b) Absolute Form:

This states that identical goods should have the same price across countries when expressed in a common currency. It assumes no transportation costs or trade barriers. It is a static concept and does not explain changes in exchange rates over time. Hence, incorrect.

(c) Expectations Form:

This relates to forward exchange rate determination and is based on market expectations about future spot rates, often influenced by interest rate differentials. It is more aligned with interest rate parity and efficient market hypothesis, not PPP. Therefore, incorrect.

(d) Contango Form:

This term belongs to commodity futures markets, where the futures price of a commodity is higher than the expected future spot price. It has no relevance to currency exchange rate theories or PPP. Thus, incorrect.

English

English 10 Questions

10 Questions 20 Marks

20 Marks 12 Mins

12 Mins