Correct option is C

The correct matching is:

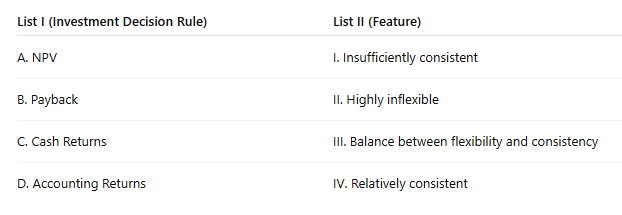

A – NPV (Net Present Value) → III (Balance between flexibility and consistency):

NPV considers the time value of money and cash flows over the project's life, offering a good balance between flexibility (evaluates cash flows at different times) and consistency (applies a consistent discounting approach).B – Payback → II (Highly inflexible):

Payback method simply looks at how quickly the initial investment is recovered, ignoring cash flows after payback and the time value of money, making it rigid or inflexible.C – Cash Returns → IV (Relatively consistent):

Cash Returns approach considers actual cash inflows and is more consistent than accounting measures because it focuses on real money, not accounting profits.D – Accounting Returns → I (Insufficiently consistent):

Accounting Returns are based on accounting profits which can vary based on accounting policies, making it less consistent and more subjective.

Information Booster:

NPV (Net Present Value):

It discounts future cash flows to the present value using a discount rate, typically cost of capital.

It reflects profitability by considering all cash inflows/outflows over a project’s life.

Balances flexibility (can adapt to varying cash flows over time) with consistency (standard discounting approach).

Widely preferred in capital budgeting due to its accuracy in evaluating investment worth.

Payback Period:

Measures time to recover initial investment without considering profitability beyond that point or time value of money.

Simple but highly inflexible, does not account for profitability or risk over full project life.

Often used as a rough screening tool but not for final decisions.

Cash Returns:

Focuses on actual cash inflows, reducing distortions caused by accounting policies.

More consistent and reliable than accounting profits for evaluating project returns.

Useful in industries where cash flow is a better indicator of performance than accounting profit.

Accounting Returns (ARR - Accounting Rate of Return):

Based on accounting profit and book values, which may not reflect true economic value.

Prone to inconsistency due to different accounting methods, depreciation, and policies.

Less preferred due to its subjectivity and lack of consideration for timing of returns.

English

English 10 Questions

10 Questions 20 Marks

20 Marks 12 Mins

12 Mins