Correct option is C

Section 80GGC of the Income Tax Act, 1961 provides a deduction for contributions made by an individual (other than a company, local authority, or artificial juridical person) to a political party or an electoral trust. This deduction is available only to taxpayers who do not claim the donation as business expenses under any other provision.

Key Points of Section 80GGC:

- 100% Deduction: The entire amount contributed to a political party or electoral trust is eligible for deduction.

- Mode of Payment: The contribution must be made through non-cash modes such as cheque, demand draft, electronic transfer, or other digital payment methods. Cash donations are not allowed for deduction.

- Eligible Political Parties: The political party must be registered under Section 29A of the Representation of the People Act, 1951.

This provision is aimed at encouraging transparency in political funding by discouraging cash transactions.

Information Booster:

Relevance of Section 80GGC:

- It applies to individuals, Hindu Undivided Families (HUFs), and partnership firms, encouraging them to donate to political parties legally.

- Companies cannot claim deductions under this section but can do so under Section 80GGB.

Additional Knowledge:

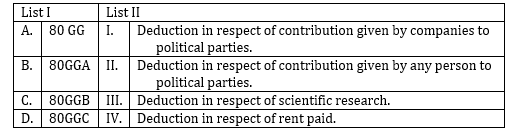

- (a) Deduction in respect of certain donations for scientific research: This falls under Section 35, which provides deductions for donations to scientific research institutions or universities.

- (b) Deduction in respect of contribution given by any company to political parties: Corporate donations to political parties are covered under Section 80GGB, not80GGC.

- (d) Deduction in respect of rent paid: Section 80GG provides a deduction for rent paid by individuals not receiving House Rent Allowance (HRA).

English

English 10 Questions

10 Questions 20 Marks

20 Marks 12 Mins

12 Mins