Correct option is B

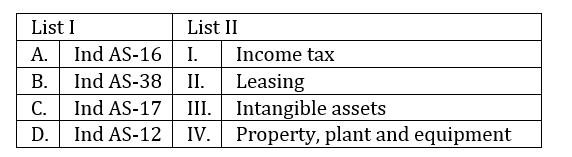

· Ind AS-16 deals with Property, Plant, and Equipment (A-IV).

· Ind AS-38 covers Intangible Assets (B-III).

· Ind AS-17 relates to Leasing (C-II).

· Ind AS-12 addresses Income Tax (D-I).

Information Booster:

· Ind AS-16 outlines the accounting treatment for tangible fixed assets, such as property, plant, and equipment.

· Ind AS-38 provides the framework for accounting for intangible assets like patents, trademarks, and goodwill.

· Ind AS-17 covers leasing transactions, including the classification of leases and the accounting treatment.

· Ind AS-12 focuses on the accounting for income taxes, including deferred tax assets and liabilities.

English

English 10 Questions

10 Questions 20 Marks

20 Marks 12 Mins

12 Mins